Today wraps up the two day FOMC meeting with the Fed statement due around 11:00 am PST followed by a press conference featuring none other than Ben Bernanke. A change to the Fed Funds rate is not anticipated. Investors will be parsing through the press release and what the Fed Chair has to say about quantitative easing. The Fed has been hands on with keeping mortgage rates at artificial lows with their purchase of mortgage backed securities.

As I write this post (7:30 am on March 20, 2013) the DOW is up 75 bps at 14531 and MBS are down about 19 bps.

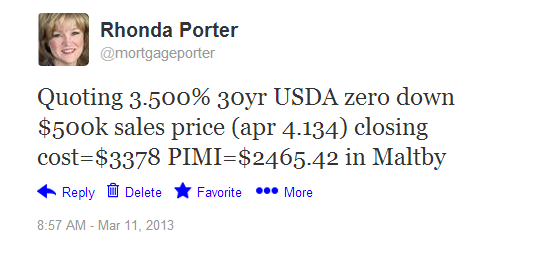

3.625% for a 30 year fixed rate (apr 3.730) is priced with 0.479 in discount points for a 45 day lock.

Stay tuned – I’ll try to do an update to this post throughout the day and we’ll see if what the Fed says influences mortgage rates today.

UPDATE: No surprises here. The Fed leaves rates unchanged and plan to continue to manipulate mortgage rates until unemployment improves. From the FOMC statement:

To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.

The Committee will closely monitor incoming information on economic and financial developments in coming months. The Committee will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. In determining the size, pace, and composition of its asset purchases, the Committee will continue to take appropriate account of the likely efficacy and costs of such purchases as well as the extent of progress toward its economic objectives.

As of 11:27 the DOW is up almost 85 points and MBS are down about 15 bps. No significant change since this morning.

12:55 pm: MBS down 37 points.

Recent Comments