EDITORS NOTE: Effective on loan applications dated October 3, 2015 and later, the Good Faith Estimate has been replaced by the “Loan Estimate” which has some similarities to the retired Good Faith Estimate, including requiring a “changed circumstance” for it to be re-issued.

Most Mortgage Originators have a distaste for Good Faith Estimate now required to be used by HUD due to a term called “changed circumstance”. A changed circumstance is the only time that a mortgage originator can re-issue a good faith estimate (unless the estimate has expired) and the only items that can be modified are those impacted by the circumstance that changed.

According to the RESPA changed circumstances is defined as:

(1)(i) Acts of God, war, disaster, or other emergency;

(ii) Information particular to the borrower or transaction that was relied on in providing the GFE and that changes or is found to be inaccurate after the GFE has been provided. This may include information about the credit quality of the borrower, the amount of the loan, the estimated value of the property, or any other information that was used in providing the GFE;

(iii) New information particular to the borrower or transaction that was not relied on in providing the GFE; or

(iv) Other circumstances that are particular to the borrower or transaction, including boundary disputes, the need for flood insurance, or environmental problems.

(2) Changed circumstances do not include:

(i) The borrower’s name, the borrower’s monthly income, the property address, an estimate of the value of the property, the mortgage loan amount sought, and any information contained in any credit report obtained by the loan originator prior to providing the GFE, unless the information changes or is found to be inaccurate after the GFE has been provided; or

(ii) Market price fluctuations by themselves

HUD adds in their RESPA FAQs (as of December 30, 2009):

None of the information collected by the loan originator prior to issue the GFE may later become basis for a “changed circumstance” upon which a loan originator may offer a revised GFE, unless the loan originator can demonstrate that there was a change in the particular information or that it was inaccurate, or that the loan originator did not rely on that particular information in issuing the GFE….

According to HUD’s RESPA FAQ 8ii, simply issuing a good faith estimate with a TBD address (or no address) is not cause for a “changed circumstance” and if a mortgage originator does issue a GFE, remember, we are presumed to have all the information necessary to create a loan application per HUD.

If a mortgage broker issues a GFE based on one lenders products and origination fees, but places the loan with another lender–the mortgage broker may wind up having to eat the difference in fees if they are higher.

Examples of things that *could* be considered a changed circumstance (after a good faith estimate is issued) according to HUDs FAQs:

- GSE (Fannie/Freddie), FHA or mortgage insurance program changes prior to the GFE being issued IF the mortgage originator did not have notice of those changes (good luck proving that).

- The property address provided by the borrower is not correct.

- Parties are added or removed from title.

- the loan does not close by the closing date in the original purchase and sales agreement provided to the lender.

- Additional appraisal, pest or other inspections requried.

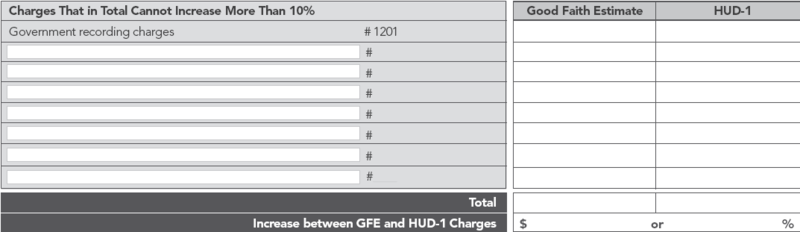

The fees in Block 1 of the Good Faith Estimate cannot change with a changed circumstance unless it is the loan amount that changed and a portion of the “origination charge” is a percentage of the loan amount. If after a GFE is issued and a changed circumstance, or borrower requested change happens, which impacts pricing (for example, a low appraisal), the change must be reflected in Box 2 of the Good Faith Estimate, which will then reflect the “adjusted origination charges”.

Changed circumstances is another great example of the best of intentions with potentially terrible outcomes for borrowers. Many mortgage originators will be weary to issue the new good faith estimate because of all the RESPA regulations it carries. In addition, banks and wholesale lenders are making their own layer of guidelines on top of the “what could trigger a changed circumstance”. Originators run the risk when issuing a revised GFE of the bank/lender balking at it down the road–especially if the borrower winds up going into default. This is just another opportunity for banks/lenders to find cause for a “buy back”.

I’m hoping by reading my articles about the new GFE, you can see why some lenders are a little leary to issue them as freely as we did pre-2010.

An important reminder that this, as well as all of my posts are my opinion only and are not intended as legal advice nor do they replace your mortgage compliance department.