Mortgage Master will be closing early today at 1:00 pm and reopening for business on Monday, January 4, 2010 at 9:00 a.m.

I wish you and yours a very Healthy and Happy New Year!

Helping Washington State homeowners learn more about their mortgage options.

Mortgage Master will be closing early today at 1:00 pm and reopening for business on Monday, January 4, 2010 at 9:00 a.m.

I wish you and yours a very Healthy and Happy New Year!

Mortgage Master Service Corporation will be closing today at noon to celebrate the holiday season. We will be reopening for business as usual on Monday, December 28, 2009.

From Mortgage Master and our family to yours Merry Christmas and Happy Holidays.

Editor's Note: We have some super talented people at Mortgage Master. This poem was written by Shelli Nixon at our office and shared during our RESPA training today. This is posted at Mortgage Porter with her permission to share with you!

T'was the week before Christmas

When all through the lands,

LO's and Closers were wringing their hands.

RESPA Changes are coming,

They all started to worry,

We'd better get trained, and trained in a hurry!

We all kept on hoping

There would be a delay.

But HUD said, "No Way," it's all here to stay.

"We love our new HUD

And our new GFE,

Don't fret, don't worry, it's as simple as can be."

We all shook our heads,

Threw our hands to the sky.

What were you smoking? You must have been high!

You took a one page doc

And changed it to three.

Easier? More simple? How can that be?

The Regs don't match up,

So now what do we do?

HUD says, "No comment, It's all up to you."

No info on TILA,

HMDA, REG B.

We are totally screwed, why can't they see??

In a time when some borrowers

Think lenders are scary,

You've given 3 pages to make them more wary.

This doesn't make sense,

Not one little bit.

We are all trying hard to not throw a fit.

So we all do our best

To put borrowers at ease.

But make more reform, please, please, please!

Please bring someone in

Who knows what to do.

What is best for both borrowers AND lenders too.

We are all still waiting,

Though not holding our breath

And hoping the government doesn't "Reg" us to death.

So on this week before Christmas,

I'd like to wish you

Good luck with RESPA, I need it too!

~Shelli Nixon, Mortgage Master Service Corporation<

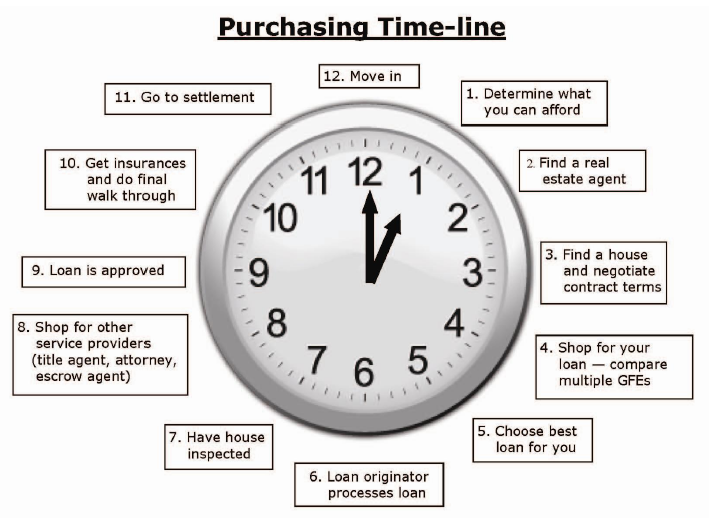

Previously I reviewed HUD's Home Purchasing Time Line, which I found several issues with if you're a home buyer in Washington State. If I'm going to pick something apart, it's only right that I offer an example of how I think it should be corrected.

Below is HUD's suggested time line.

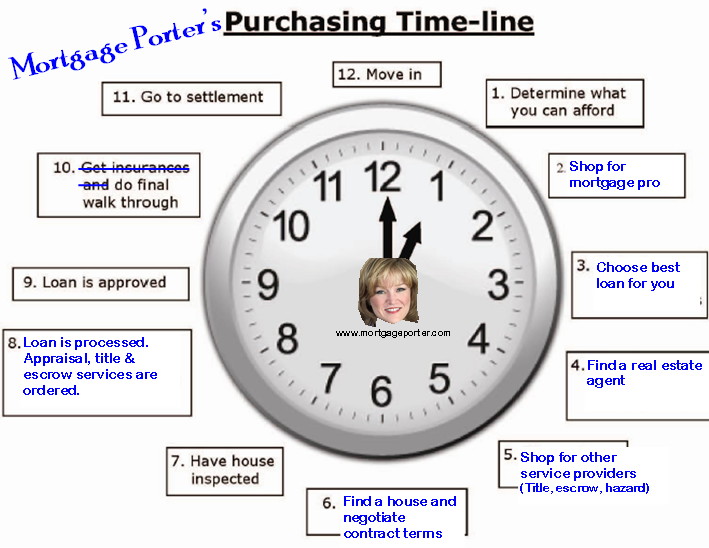

Here is how I see a successful purchase transaction evolving. My modifications to HUD's time line are in blue below.

Rhonda Porter's Ideal Home Purchase Time Line

Step 1: Determine what you can afford. Make sure you really consider how much home you can personally afford (not just how much home you qualify for or what a lender tells you). Please do not stretch yourself to be "house poor". Keep in mind the lessons that this economy is teaching all of us.

Step 2: Shop for a mortgage pro. Oh how I wish that instead of a shopping cart for rates (which is a moving target) and fees on page 3 of the new Good Faith Estimate, that it had a place for you to "shop" your mortgage professional instead. Perhaps a place where you could compare resumes and available products instead of focusing so much on rate and fee. The person who will be guiding through the process of obtaining one of the largest debts you may have in your lifetime should not be selected so casually.

Step 3: Choose the best loan for you. After selecting your mortgage professional; he or she should consider your financial goals and help provide you with information to allow you to make an educated decision on which mortgage program best suits your goals based on what you currently qualify for. You need to know what your total payment will be and how much money will be required for your down payment and closing costs BEFORE you start looking for your next home.

Step 4: Find a real estate agent. I recommend asking friends and family members who have recently purchased or sold a home and interview them. If you need a recommendation for one around the greater Seattle area, please ask me!

Step 5: Shop for other service providers. This has to happen BEFORE you prepare an offer on your next home assuming your lender permits you to shop (this is per RESPA guidelines–not a control freak mortgage originator). If you select your own title and escrow service provider, there is no cap to how much their fees can change at closing. If you use the providers from the mortgage originators preferred list, the accumulative fees at closing cannot exceed 10% from the good faith estimate.

Step 6: Find a home and negotiate contract terms. Now you can start searching for your next home with confidence since you know what you can afford and you have your home buying team assembled.

Step 7: Have house inspected. I recommend this even if your home is new construction. I can tell you a few stories…but this post is all ready getting too long!

Step 7.5: Shop and select your home owner insurance provider. Do not wait until closing to do this. Home owners insurance rates can vary and your credit score will impact your insurance rate. Also if the home has a history with certain insurance claims, there could potentially be issues that are better to be aware of early in the process.

Step 8: Loan is processed. Once we have a signed around agreement, your loan is processed and various services are ordered or set up. This is also the time to review you lock options to determine whether you want to commit to an interest rate or float (not lock).

Step 9: Loan is approved. The loan approval may come back with conditions. This happens after the underwriter reviews what has been submitted to them during the processing period.

Step 10: Do the final walk through.

Step 11: Go to settlement. Prior to your escrow appointment, I recommend that you obtain a copy of your estimated HUD-1 Settlement Statement 1-2 days in advance so that you have time to review the final figures. Be sure to let your mortgage professional and escrow officer/settlement agent know that you expect this as the lender will need to provide your loan documents to the closing company a few days earlier than "the norm". The same is true if you want a complete copy of your loan documents to review prior to your signing appointment.

Step 12: Move in! Yay–this can be such an exciting time! Typically there may be a few days between signing your closing documents and moving into your new home.

HUD has unveiled their new "Shopping for your Home Loan – HUD's Settlement Cost Booklet". What was once a ppamphlet that was included with your loan application has been replaced by a 49 page booklet. This revised guide for borrowers was created to accompany HUD's new Good Faith Estimate which goes into effect on January 1, 2010.

HUD's new guide is to help consumers navigate the new Good Faith Estimate. I'm not going to go all the way through it on this post, I do want to point out issues with HUD's Home Purchasing Time Line (which you'll find on page 4).

Do you see anything wrong with this picture? Let's review step by step.

1. Determine what home you can afford. I agree with this. What home you can afford may be different than what home you qualify for. You don't have to buy as much home as you may qualify for and you might qualify for less than you desire. What's most important is being able to afford the home. I think this step is referring to doing some serious gut checking and reviewing of your personal budget BEFORE meeting with a real estate agent or mortgage originator.

2. Find a real estate agent. I think step two should be to find a mortgage professional instead of the agent. They have the cart before the horse with this step. The last thing a home buyer needs is to be shown a bunch of home they may not qualify for. Meeting with a mortgage originator first will help them narrow down what programs they qualify for that will suit their financial needs (I think this is HUD's Step 5). Agents may debate me on this because they like to direct buyers to their preferred lender.

3. Find a home and negotiate the terms. This is unbelievable! HUD is recommending that you enter into a binding contract before knowing if you're approved for the mortgage. Yes there are financing contingencies, but you do not tie up a seller's property when you don't even know that you can close on a transaction. Plus, most real estate agents will not show you a home until you have been preapproved by a mortgage professional.

4. Shop for your loan — compare multiple good faith estimates. This is very flawed. HUD's new good faith estimate carries RESPA reform which in a nutshell means that if a mortgage originator provides a borrower a good faith estimate, they are presumed by HUD to have obtained enough information from you to have created a loan application. This creates a certain amount of liability for the mortgage originator that in this day and age, most will not accept. Not to mention that rates change constantly, sometimes several times a day. If anything, you should shop for the most qualified mortgage professional and not "the loan" or rate…this step should take place around Step 2.

5. Chose the loan that's best for you. This should take place at step 2 or 3 (after you select your mortgage professional). This is too late in the game to be determining your financing.

6. Loan originator processes the loan. Your mortgage originator begins processing your loan at application for purposes of preparing your preapproval letter. Your loan may actually go into processing and underwriting once you are proceeding with your transaction.

7. Have house inspected. This typically take place after you find your home and have negotiated your contract. You're not going to want to be paying for an appraisal (which would take place at processing) if your potential home doesn't pass inspection.

8. Shop for other service providers (title, attorney, escrow agent). Is this a HUD after thought? If you are going to shop for your title or escrow, you're going to need to do this prior to the contract being written as the purchase and sales agreement dictates who the providers will be (unless the agent writes "buyers choice"). Plus, HUD's new GFE dictates how much the title and escrow fees can change at closing based on if you shop or if you allow the lender to select these service providers.

9. Loan is approved. There are different steps of loan approval. This is most likely "final loan approval" meaning all conditions (documentation) have been provided and reviewed by underwriting.

10. Get insurances and do final walk through. I recommend shopping and selecting your home owners insurance much earlier in the process. Once you have a bona fide contract and your home has passed inspection, you can start shopping for your insurance agent.

11. Go to settlement. In Washington, you're probably going to your signing appointment at the escrow company a couple days before closing. Sometimes signing will feel like it's at the eleventh hour!

12. Move in.

Watch formy next post where I share how I think this purchasing time line should look.

I have been wondering how HUD’s new GFE, which goes into effect on January 1, 2010 will impact title and escrow companies. It appears as though HUD would like to see the borrower have the possibility of more control in selecting those services instead of the current system where typically in our area of Washington, either the real estate agents thumb wrestle over their favorite title or escrow company or the lender may select. Rarely does the consumer have a voice in who will be providing the title insurance on their home or who will be the “neutral third party” facilitating the closing one of their largest transactions in their lifetimes.

From a local escrow and title provider The Talon Group’s blog:

The current local practice of the seller choosing title insurance appears to be at odds with HUD reform that attempts to put the buyer back in the drivers seat. HUD makes no bones about it’s intentions for empowering buyers to shop for the best deal possible when choosing title and settlement services. Also going into effect January 2010, lenders will face strict guidelines and tight tolerances when listing these services on the new Good Faith Estimate.

The “tolerances” define what the variance in costs for title and escrow/settlement services may be between the (soon to be) binding good faith estimate and the settlement statement at closing. The tolerances for title and escrow fees fall into a couple “buckets”:

10% tolerance:the accumulative fees for title and escrow services cannot exceed higher than 10% of what was disclosed on the good faith estimate.

Not subject to tolerance; there is no limit to what the difference may be at closing verses what was disclosed on the good faith estimate.

With these tolerances set forth on the new good faith estimate, I wrote an article at Rain City Guide predicting that the big banks will use the new Good Faith Estimate as a reason to mandateto their mortgage loan originators they must only use their “in-house” or affiliated providers and may not recommend outside escrow or title companies for service–regardless of established relationships or a proven track record of excellent service. I believe this will follow in the footsteps of HVCC where banks are using AMCs (appraisal management companies) that they have ownership interest in–even if the HVCC fiasco is fixed, I think you’ll see banks still insisting that an AMC is used and will use the new GFE to gain title and escrow revenue. They’ve tasted the gravy.

I feel so fortunate to be working for a mortgage company that is flourishing during this historic times in the mortgage industry. I credit part of our success to the fact that we leaned towards the conservative side during the "subprime boom years". It was not unusual to have bank and wholesale lender reps to say to me, when pitching their products, "I can't believe your office isn't doing options ARMs; do you know how much money other LO's are making at other offices?" Don't get me wrong, there can be scenarios where subprime or exotic mortgages may make sense–but to dish them out to consumers with the main purpose of padding your pockets is wrong. I digress…and I may write a post about this topic later.

Mortgage Master Service Corporation is treating their employees to our annual Christmas – Holiday Party which will begin at around 11:30 am Friday, December 11, 2009. Our office will reopen for business as usual on Monday, December 14, 2009.

Happy Holidays and thank you for your loyal continued support on behalf of everyone at Mortgage Master.

I've been noticing at my bank a new promo offering "1% mortgage cash back". My husband has enjoyed teasing me saying stuff like "why would anyone use you?" And when he was at the bank branch, he asked a mortgage-teller if this was legit they replied something along the lines of "yeah, isn't this great!"

Today I received my monthly bank statement and sure enough, stuffed inside was an advertisement for the "1% mortgage cash back. The bold print states that "you will receive 1% of your principal and interest payment back each year!"

But it's the fine print you need to read…by the way, the fine print takes up about 30% of this add…you really have to read everything word by word. In the middle of the print, I found what I was looking for:

"There is a $500 calendar year cap on the principal reduction and cash back amount…" and by the way, you must have (or get) a checking account with this bank in order to get up to $500.

And it get's better…when I priced out a refinance scenario based on excellent credit, a $400,000 loan amount and a home valued at $500,000; I was quoted 0.25% higher in rate than what I would offer today on a 30 year fixed rate (4.625%/APR 4.777). Serious. That bank is making pretty darn good change on that extra quarter point in interest while giving the consumer back a maximum of $500 per year.

In my opinion, this is a terrible way to potentially trick consumers into thinking they're getting back much more than $500. To me, 1% of your mortgage sounds like 1% of your loan amount and with this promo, it's not.

A quarter point interest rate difference on a $400,000 loan amount will pay you about $60 per month or $720 a year! Not to mention interest paid over the life of the loan.

My advice, work with someone who can offer you a more competitive ratedon't chase a bad gimmick from a bank.

![]() Rhonda Porter is a Licensed Mortgage Originator MLO121324 living in the greater Seattle area. Rhonda began her career in 1986 in the title and escrow industry and began her mortgage career in 2000. She enjoys helping people understand the mortgage process and started writing The Mortgage Porter in late 2006. Read More…

Rhonda Porter is a Licensed Mortgage Originator MLO121324 living in the greater Seattle area. Rhonda began her career in 1986 in the title and escrow industry and began her mortgage career in 2000. She enjoys helping people understand the mortgage process and started writing The Mortgage Porter in late 2006. Read More…

{kind=link}

Recent Comments