Following the release of the QM and Ability to Repay rules from CFPB, I decided to try to read through the proposed Loan Originator Compensation rules. I found this pretty interesting. Instead of making additional regulations for Mortgage Originators who work at banks or credit unions, why not just make them subject to the SAFE Act and require them be licensed?

Archives for January 2013

Waiting for HARP 3.0? You can sign this Petition.

January 15, 2013 by 49 Comments

A petition to remove the securitization date with HARP 2.0 is making it’s way through social media. Currently, in order for a mortgage to qualify for a Home Affordable Refinance (HARP 2.0), the mortgage needs to have been securitized by Fannie Mae or Freddie Mac prior to June 1, 2009. Securitization has nothing to do with when a loan closed and it often takes place weeks or sometimes months after closing.

Many home owners have felt burned by this cut-off date as they have no control over when Fannie or Freddie securitized their loan yet they’re being punished by not being allowed to use this program to refinance.

The petition is also asking the home owners who have already refinanced using the HARP program, to be allowed to “re-HARP” or refinance again under the HARP program.

Click here for more information about the Home Affordable Refinance Program (HARP).

Congress and the Obama Administration has been discussing the possibility of changing guidelines to the Home Affordable Refinance Program, including removing or extending the securitization date among other things. The revamped program, which may also be open to loans not securitized by Fannie or Freddie, has been referred to HARP 3.0 or #MyRefi.

The petition was created last week is trying to reach 25,000 signatures by February 8, 2013.

Under the Home Affordable Refinance Program (HARP) The Director of The Federal Housing Finance Agency has authority to extend or eliminate the eligibility cutoff date. Currently the date is set as 5/31/09. Many responsible home owners are unable to take advantage of the program to reduce their mortgage rates because of this date. On 3/17/12 HARP was revamped (HARP 2.0) and home owners were given the power to shop for the best rates. However, those who previously refinanced under the original program are not eligible because of the the arbitrary cut off date and 1 time use limit set by FHFA Director Edward DeMarco. Eliminating the cutoff date and allowing home owners a 2nd chance to refinance under HARP 2.0 would help millions of Americans to save money on their monthly mortgage payment.

Mortgage rate update for the week of January 14, 2013

January 14, 2013 by Leave a Comment

This week is packed with economic reports that may impact the direction of mortgage interest rates. Mortgage rates are based on mortgage backed securities (bonds). When the Fed minutes revealed hints that the FOMC may stop purchasing mortgage backed securities last week, mortgage rates ticked slightly higher. However Japan is hinting of buying US bonds, which is helping rates trend lower this morning.

Signs of inflation or the economy recovering may also cause mortgage rates to trend higher. Here are some of the economic indicators scheduled to be released this week:

- Mon, January 14: No scheduled data – however, Ben Bernanke is speaking this afternoon on monatary policy.

- Tue, January 15: Producer Price Index (PPI), Retail Sales and Empire State Index

- Wed, January 16: Consumer Price Index (CPI) and the Beige Book

- Thurs, January 17: Initial Jobless Claims, Building Permits, Housing Starts and Philadelphia Fed Index

- Fri, January 18: UoM Consumer Sentiment Index

NOTE: Monday, January 21, 2012 our office will be closed in observance of Martin Luther King Day.

As I write this post (8:24 am pst) the DOW is up 5 at 13493 and MBS for the FNMA 30 year is up slightly.

If you would like a mortgage rate quote for your Washington state home, please click here. I’m happy to help!

A Strategy for Seattle Home Buyers: I Love Your Home Letters

January 12, 2013 by 2 Comments

The Wall Street Journal writes about a strategy home buyers in hot housing markets are using to get their offers accepted in hotter housing markets. From WSJ:

“In an echo of the last housing boom, ardent pitch letters from eager home buyers are popping up again in hot U.S. real-estate markets like Silicon Valley, Seattle, San Diego, suburban Chicago and Washington, D.C., housing economists and real-estate brokers say.

The heartfelt missives, often accompanied by personal photos, aim to create an emotional bond that can give their writers an edge—especially in situations where multiple bidders are vying for the same house. And the reappearance of buyer pitches, also known as love letters, offers further evidence that the housing market is rebounding after a five-year slump.”

I have written letters to underwriters before on behalf of my borrowers and have gone so far as to include a photo of my client which has helped with loan approvals. A letter from the buyer to “pitch” their story to the seller is something I haven’t heard of before.

What is probably more important than “a pitch letter” to the seller is your preapproval letter from a respected mortgage professional. A preapproval letter will assure the seller that you are approved for a mortgage specific to your offer and that the transaction should successfully close. A well written preapproval letter addresses the borrowers down payment, credit, income and employment have been verified.

In a multiple offer situation (sometimes referred to as a “bidding war”) it’s not unusual for the seller’s real estate agent to call the mortgage originator who has written the preapproval letter to do a “sniff test”.

While a letter from a potential home buyer expressing how perfect the home is for their family may give a buyer an edge over other offers, please don’t forget your mortgage preapproval letter.

If you are considering buying a home in Seattle or anywhere in Washington state, where I am licensed, please contact me. I would love to help you with your mortgage!

CFPB’s Qualified Mortgage Rule and the Ability to Repay

January 10, 2013 by 10 Comments

Today the CFPB released the “ability-to-repay” and “qualified mortgage” rule which is set to go into effect next year on January 10, 2014. These new laws will require that lenders consider a borrowers ability to repay a mortgage.

Should I refi my 15 year fixed mortgage if my rate is 3.250%?

January 8, 2013 by Leave a Comment

I’m reviewing a scenario for one of my returning clients who currently have a 15 year fixed mortgage at 3.250% from when they purchased their Seattle home 1.5 years ago. The current balance is around $387,600 with a principal and interest payment of $2930.13. They do not have taxes and insurance included in their mortgage payments. My clients are considering another 15 year fixed mortgage or possibly a 10 year fixed mortgage.

Quotes below are with impounds waived (lenders typically charge 0.25% in fee when taxes and insurance are paid by the borrower instead of included in the monthly mortgage payment). Rates are based on mid-credit scores of 740 or higher and a loan to value of 80% or lower. Mortgage rates are as of January 8, 2013 and may (and will) change at any time.

2.875% for a 15 year fixed (apr 2.979) has a rebate credit which brings the estimated net closing cost down to $1229 based on a loan amount of $389,000. The principal and interest payment is $2663.04 reducing their monthly mortgage payment by $267.09.

2.750% for a 15 year fixed (apr 2.886) has closing cost estimated at $4195. The principal and interest payment is $2660.20 with a loan amount of $392,000. This scenario reduces their payment only slightly more to $269.93. If it were my choice, I’d opt for the slightly higher rate with lower closing cost.

Currently, the 10 year fixed rate for this scenario is actually priced slightly higher than the 15 year fixed.

2.875% for the 10 year fixed (apr 3.020) with $1700 in net closing cost after rebate credit. The principal and interest payment would be $3,733.81 based on a loan amount of $389,000.

Again, I would opt for the 15 year at 2.875% as the pricing is slightly better and I could always make the additional principal payment of $1070.77 (3733.81 less 2663.04) in order to pay down my mortgage in 10 years vs 15.

If you are interested in refinancing or buying a home located anywhere in Washington state, please contact me.

Mortgage update for the week of January 7, 2013

January 7, 2013 by 2 Comments

This week may seem like a real yawn with only the initial Jobless Claims being released on Thursday, January 10, 2013.

On Thursday we may hear from the Consumer Protection Financial Bureau’s about what defines a “qualified mortgage” (QM). From Bloomberg:

The qualified mortgage rule, mandated by Congress as part of the 2010 Dodd-Frank Act, is aimed at tightening lax underwriting that fueled the housing bubble. The regulations aim to protect consumers from mortgages they cannot afford by requiring lenders to take steps such as verifying income and assets. In return, lenders gain some protection from lawsuits.

Although having a “qualified mortgage” may sound like a does of common sense, we won’t know what we are dealing with until we learn about what constitutes a “qualified mortgage”. For example, currently an industry standard for a debt-to-income ratio is 45%, should the government decide that a DTI of 43% is required in order to be deemed a “qualified mortgage”, many Americans will find themselves not able to obtain a mortgage OR possibly paying a higher rate or fee for a “non-qualified” mortgage. I’m anxiously awaiting Thursday’s news from the CFPB.

If you are interested in refinancing or buying a home in Bellingham, Bellevue, Bainbridge Island or anywhere in Washington, I’m happy to help you!

Reader Question: WHEN did Fannie Mae securitze my mortgage?

January 5, 2013 by 1 Comment

This question is from a comment on one of my blog post addressing HARP 2.0’s eligibility date (Home Affordable Refinance Program), which many home owners have found to be a source of frustration. In order to qualify for the HARP 2.0 program, the mortgage must have been securitized by Fannie Mae or Freddie Mac prior to June 1, 2009. Securitization takes place after the closing of the loan and is completely out of the borrowers control.

This person is being told their loan was securitized YEARS after it closed in 2003. It is possible that the lender had to wait a long period of time before being able to sell the loan to Fannie.

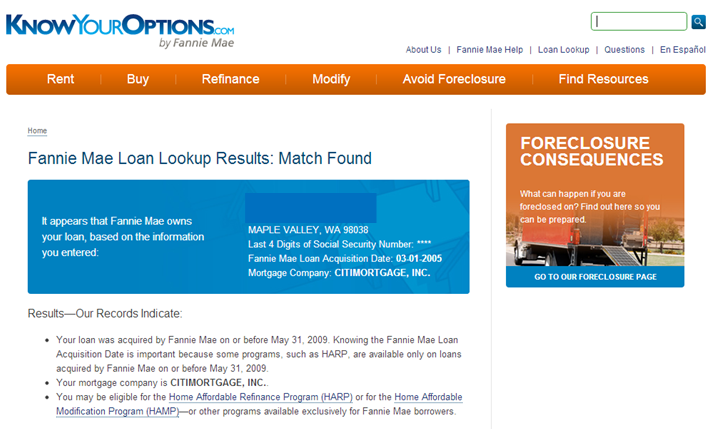

I highly recommend checking Fannie Mae’s site at https://www.knowyouroptions.com/loanlookup to verify if and when your mortgage is securitized by Fannie Mae.

Fannie Mae recently made improvements to their loan lookup site with getting rid of their terrible (sometimes comical) “bot” filter by replacing it with the borrowers last four of their social.

You will need to enter in the information of the primary borrower from when the mortgage was obtained. The site can be picky as to your address, for example, Ave vs Avenue; so you may have to try re-submitting your information.

“Match Found” means that Fannie Mae shows they have a mortgage on this property and that it may qualify for HARP 2.0. The improved site also provides the date the loan was securitized. A “match found” response does not guarantee that someone will qualify for the HARP 2.0 refinance program.

Back to my reader…

Should you verify with Fannie Mae’s site that your property was securitized with Fannie Mae prior to June 1, 2009, I would contact a local licensed mortgage professional to help you with your HARP 2.0 refinance.

I’m not sure what “independent site” was used to verify. Fannie Mae’s site would be the ONLY site I would use for verification of a Fannie Mae securitized mortgage.

Should you find that your mortgage was securitized after the June 1, 2009 cut-off date, you may have to wait and see if Congress passes HARP 3.0 (aka #myrefi) which hopefully will remove the cut-off date.

In my opinion the cut-off dates with the HARP 2.0 programs are hurtful for consumers who had no control over when their mortgage was securitized by Fannie Mae or Freddie Mac. I hope HARP 3.0 is available soon. When and HARP 3.0 is available, I will be sharing that information here on my blog.

By the way, Freddie Mac also has a website for verifying if your mortgage was securitized by Freddie. If your conforming loan was not securitized by Fannie Mae, the next step is to try Freddie Mac’s site to look up your loan: https://ww3.freddiemac.com/corporate/ Fannie Mae has a majority of the “market share” which is why I recommend trying Fannie Mae first.

If your home is located anywhere in Washington State, I’m happy to help you with your HARP(or any) refinance.

Recent Comments