I’m receiving notices from a couple of the lenders we work with that they are temporarily increasing rate lock extension fees due to Fannie Mae’s increased guarantee fees (LLPA) that will hit us in 2014. An extension fee is an additional cost that may be charged in order to keep a rate locked when the rate lock is expiring.

Major Lender Increases Cost to Extend Rate Lock Commitments

August 7, 2012 by 3 Comments

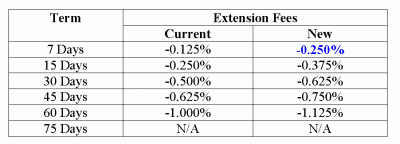

Yesterday we received a memo from one of the big 3 banks notifying us of an increase to extension fees on all conforming mortgages on locks effective August 9, 2012 by 0.125%. An extension fee is an additional cost associated with extending the rate lock period of your mortgage loan. For example, if your loan is locked for 30 days, and it takes more than 30 days to close the loan, there will more than likely be a fee to extend the rate lock commitment long enough to close the transaction. Just like a rate lock, the longer the time period that is needed, the higher the cost is. It is typically more cost effective to have a longer lock period than to pay for an extension.

Each lender we work with has their own rate lock and extension policies. Here is what it cost to extend with this lender:

It’s important to note that this is NOT Mortgage Master Service Corporations general extension fees. We work with several lenders and what ever their fees are to extend are passed on to the transaction. One lender that we work with currently offers extensions on a daily basis (instead of blocks of time) so at a cost of 0.025% per day. If we only need 5 days for an extension, the cost would be 0.125%.

Everyone likes to keep cost down and avoid extension fees. This is why it’s critical to provide your mortgage professional with requested documentation promptly, especially once your loan is locked.

Extensions: When Your Time is Up on Your Lock

August 20, 2008 by 2 Comments

When you lock in a mortgage interest rate, it is for a specific period of time, such as 30, 45 or 60 days. Your mortgage professional should make sure it is for an adequate amount of time to close the transaction. If it’s a purchase, the lock may be for a few days after the transaction and if it’s for a refinance, 30-45 days should be plenty of time in a “normal” market for the lock period. Purchases, depending on the type of transaction can be closed from two weeks or more (or more is preferred, less can happen too).

When you lock in a mortgage interest rate, it is for a specific period of time, such as 30, 45 or 60 days. Your mortgage professional should make sure it is for an adequate amount of time to close the transaction. If it’s a purchase, the lock may be for a few days after the transaction and if it’s for a refinance, 30-45 days should be plenty of time in a “normal” market for the lock period. Purchases, depending on the type of transaction can be closed from two weeks or more (or more is preferred, less can happen too).

Mortgage Interest Rate Locks 101

May 8, 2007 by 22 Comments

EDITORS NOTE: With changes to the 2010 Good Faith Estimate, a lot of the information below is no longer relevant (relating to the GFE). However, the pricing is still a good example of how locks work.

I love it when I’m asked an excellent question from a potential client. This person  is still shopping for his next home and who the lender will be to provide financing. At this point, I have provided several good faith estimates and a total costs analysis to compare possible scenarios side by side along with how the mortgages may be working for him in 5 and 10 years.

is still shopping for his next home and who the lender will be to provide financing. At this point, I have provided several good faith estimates and a total costs analysis to compare possible scenarios side by side along with how the mortgages may be working for him in 5 and 10 years.

Here are a few of his questions:

What level of guarantee can you offer me with these rates you have provided on the Good Faith Estimates?

Until your loan is “locked” the interest rates on the Good Faith Estimate (GFE) is simply a reflection of what the rate is at the moment the Loan Originator prepared the GFE. In fact it’s possible that the rate may have changed just moments after the GFE was provided to the client. Mortgage interest rates can change throughout the day. The GFE is not a guarantee of the mortgage interest rate, costs or that one is qualified or approved for a loan program. (I have addressed guarantees towards the of this post).

Can I lock in my rates and closing costs before I find my new home?

Typically, the buyer has a signed around (agreed to) purchase and sale agreement. Most locks require a property address along with the borrowers full legal name, social security number, program type, purchase price/loan amount and credit scores along with the length of time required to close the transaction.

Some lenders, like Mortgage Master, have a “lock and look” feature which does allow buyers to lock their interest rate before finding their next home. Unless the market is experience ramped rate increases, I recommend not doing this. The locks are for longer terms (so they are more expensive) and should rates improve, odds are the buyer is not going to want the long term rate they’ve committed to with the lock.

How long is the lock period?

Locks have various time periods that are available to accommodate a borrowers needs. The most common for a purchase is a 30 or 45 day lock. Again, loans are locked in based on how many days are needed to accommodate the transaction closing date. The longer the lock period, the higher the costs is for a specific rate.

For example, here is what the difference in fee may look like based on various lock times assuming the 30 day lock is par or neutral (comparing the other locks to 30 days):

- 15 day lock = 0.125 better over the 30 day price

- 30 day lock = 0

- 45 day lock = 0.05 cost over the 30 day price

- 60 day lock = 0.150 cost over the 30 day price

- 70 day lock = 0.270 cost over the 30 day price

- 90 day lock = 0.400 cost over the 30 day price (may have to pay additional upfront lock fee for this long of term)

So if you have a loan amount of $400,000 and a closing date that was just shy of two months away, and you want to have the 30 day rate, the cost may be $600 (400k x 0.15). If you have a longer closing, a Mortgage Professional should advise you of your options of locking now or waiting until your close date is more near and what the risk are (rates changing). At 70 and 90 days, instead of paying an increased cost for the 30 day rate, you could also opt for a slightly higher rate (0.125%) and still have the 30 day pricing (it would be factored into the rate). Again, the above numbers are just an example of possible pricing. Rates and pricing do change constantly.

You can lock 90 days and beyond. However, the cost increased (as you can see from my figures above) and there is often an additional upfront lock fee that is non-refundable.

Click here for your rate quote for homes located in Washington.

It’s important that the loan is locked in for the right amount of time. If a loan does not close before the lock expiration date, the lender is put in a position to where they may need to extend the lock. The price of a lock extension varies from lender to lender and, if the market has improved from when the loan was originally locked, there may not be a cost for a shorter extension. Some lenders charge 0.015 per day of the extension; so if 10 more days were required to close and fund the loan, the cost could be 0.15% (0.015 x 10 days) of the loan amount. On a $400,000 loan amount, this is an additional cost of $600. You can see why it’s important to lock your loan correctly in the first place.

not close before the lock expiration date, the lender is put in a position to where they may need to extend the lock. The price of a lock extension varies from lender to lender and, if the market has improved from when the loan was originally locked, there may not be a cost for a shorter extension. Some lenders charge 0.015 per day of the extension; so if 10 more days were required to close and fund the loan, the cost could be 0.15% (0.015 x 10 days) of the loan amount. On a $400,000 loan amount, this is an additional cost of $600. You can see why it’s important to lock your loan correctly in the first place.

I recommend that when you lock in your loan, you ask your Mortgage Professional to guarantee the closing costs associated with the loan. Third party costs, such as the appraisal title and escrow fees, the Mortgage Professional has no control over. I would not work with any Loan Originator who is not willing to stand by their closing costs. As a borrower, you should be able to bring your Good Faith Estimate with you to closing (your signing appointment) and have the lender’s fees be reasonable close.

Once you have locked in your loan, you should receive:

-

Written lock confirmation stating what the rate and points are associated with that rate.

-

Request an updated Good Faith Estimate (and ask the lender if they are going to guarantee their loan costs) to correspond with the lock. [2010 UPDATE: You may find that mortgage originators will provide a written rate quote prior to providing a Good Faith Estimate with an actual Good Faith Estimate to follow.]

What ever you do, please do not select the person who will be assisting you with your largest investment (your mortgage) by interest rate alone.

Recent Comments