If we mortgage originators had more flexibility of when a good faith estimate could be revised for our clients, I would be applauding the last page of the revised HUD-1 Settlement Statement. On this page, the borrower actually get to compare the closing costs on the good faith estimate directly to the those shown at closing on the estimated HUD-1 Settlement Statement side by side. My beef is that we are very limited by HUD's grey definition of "changed circumstances" which allows us to issue an updated good faith estimate.

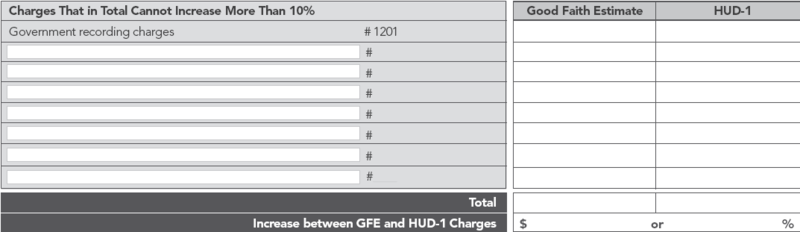

The page 3 of the HUD-1 also breaks the fees into the various tolerance levels. The first section has the fees that cannot increase. If the HUD-1 fees in the right column are higher than those in the Good Faith Estimate column on the left, the mortgage originator will have to refund the difference.

The next section has the fees where HUD will allow an accumulative variance of up to 10%.

Followed by the last section where the tolerance does not apply. The fees shown in the section below can change from the good faith estimate.

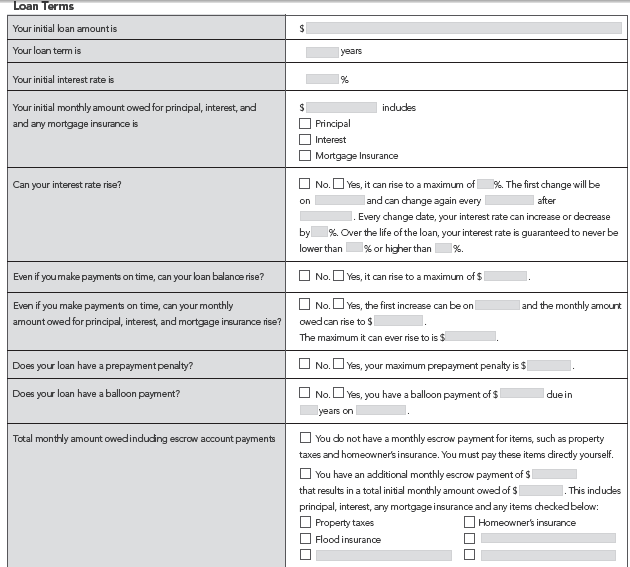

Page 3 of the HUD-1 Settlement Statement concludes with a summary of the loan terms. Hopefully none of these terms (or fees) are a surprise to the borrower, their mortgage originator should have explained the details fully well in advance of the signing appointment.

Ideally, mortgage companies will provide loan documents a few more days in advance than what is taking place with our current GFE/HUD and RESPA guidelines…this means longer transaction times for consumers. I also highly recommend that consumers obtain a copy of their estimated HUD-1 Settlement Statement two days before their scheduled signing appointment.

I've always recommended that borrowers bring their good faith estimate with them to their signing appointment, maybe now they won't need to!

Discover more from The Mortgage Porter

Subscribe to get the latest posts sent to your email.

Please leave a reply