No surprise that the FOMC is not making any changes to the Fed Funds rate. What may have surprised some is the Fed’s focus on trying to keep mortgage rates low with it’s purchase of mortgage backed securities. From today’s press release:

To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee agreed today to increase policy accommodation by purchasing additional agency mortgage-backed securities at a pace of $40 billion per month. The Committee also will continue through the end of the year its program to extend the average maturity of its holdings of securities as announced in June, and it is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities. These actions, which together will increase the Committee’s holdings of longer-term securities by about $85 billion each month through the end of the year, should put downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.

….If the outlook for the labor market does not improve substantially, the Committee will continue its purchases of agency mortgage-backed securities….

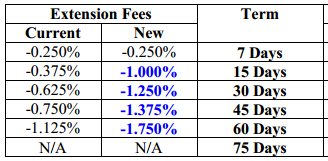

The efforts to keep mortgage rates low will be in contrast to the increase in the “g-fees” by Fannie Mae and Freddie Mac. It will be interesting to see how much of an impact the Feds efforts will make.

Stay tuned for Ben Bernanke’s press conference happening in a few hours. Meanwhile… let’s twist!

Recent Comments