When you apply for credit, it may appear as an inquiry on your credit report even if you decide not to proceed with the credit or debt you applied for. The credit reports that mortgage companies use will show the inquiries going back 120 days.

When you apply for credit, it may appear as an inquiry on your credit report even if you decide not to proceed with the credit or debt you applied for. The credit reports that mortgage companies use will show the inquiries going back 120 days.

Why does a lender care if you have credit inquiries – even if you never proceeded to take the credit that was offered to you? Inquires to your credit appears as though you are shopping for credit and therefore may be taking on additional debt. Additional debts may impact your ability to make payments on your new mortgage.

Lenders will require that a borrower write a “letter of explanation” addressing each individual inquiry including whether or not new credit was obtained. They want to know “why” the borrower was looking at possibly getting credit and “if” they indeed did obtain new credit that possibly is not yet showing as a debt on the credit report.

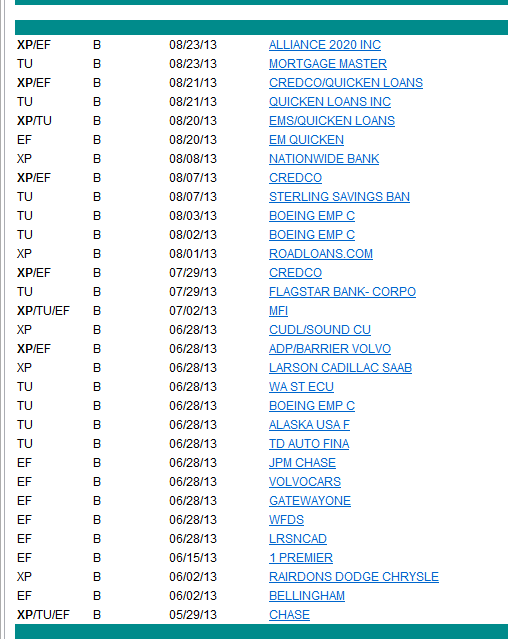

On this list of inquiries, you can see that in May, the person was shopping for a car. If they did buy a car and have a new debt that is not yet reflected on the credit report, they will need to have the new car payment added to the loan application and be re-qualified with that payment. (Please DON’T buy a car when you’re getting ready to buy a home).

Lenders will do a “soft pull” of a borrowers credit just prior to closing which will also review a borrowers inquires again to make sure no new debts have been obtained during the loan process.

Credit inquires may also ding your credit scores. The more inquiries you have in a short period of time, the more impact it may have to your score. Borrowers are supposed to only be dinged one time when allowing mortgage companies to pull credit within a short period (30 days, I believe) of time.

If you are considering buying or refinancing a home anywhere in the state of Washington, I’m happy to review your credit with you and help you with the loan process. Click here if you would like me to provide you with a mortgage rate quote.

Speak Your Mind