Mortgage originators (also referred to as Loan Officers or MLOs) are required to be licensed with the NMLS unless they work for a depository bank or credit union, in which case they are only required to be “registered” (per the SAFE Act).

Mortgage originators who are licensed renew their license annually. In Washington State, our license expires at the end of the calendar year. In order to renew a license, a Washington State MLO (loan officer) needs to complete a total of 10 hours of certified education and “attest” their records with the NMLS.

MLO’s wanting to originate mortgages in Washington in 2013 (now!!!) need to have a valid license to do so. If they (or their employers) delayed meeting the licensing requirements, they cannot take an application until they have renewed their license for 2013. This from an email I received from DFI:

Monday, December 31, all non-renewed Washington licenses expire. This means those companies, branches or individuals who don’t have an approved renewal can no longer operate in Washington…

DFI reports that for MLO’s originating in Washington State, who are licensed, currently “81% are renewed which represents 6,816 individuals.” It will be interesting to see how many MLO’s either opt to work for a bank or credit union, where they can be gravy fed, or elect to find a new career. With increased compliance regulations, I know of several LOs who find the frustration of layers of disclosure requirements untolerable.

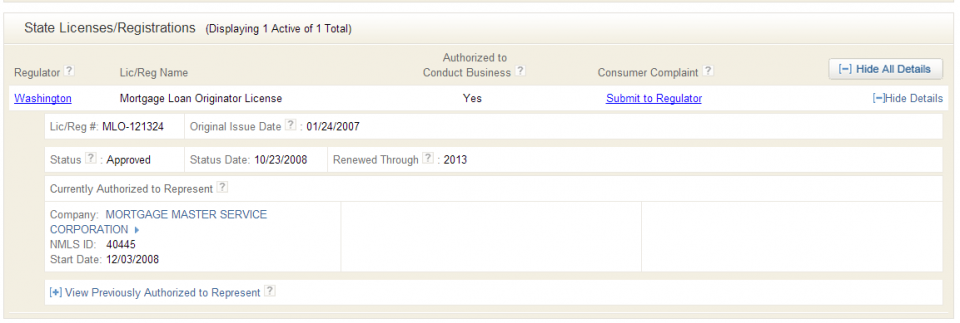

To verify if your MLO has a current license, you can visit www.nmlsconsumeraccess.org and search their name or license number. Scroll to the bottom of the page after you have selected your MLO and you can see how long their license is valid for OR if they are “registered” and not actually licensed.

I am licensed through 2013 to originate mortgages on homes located anywhere in Washington State. If you’re interested in buying a home or refinance, please contact me!

Discover more from The Mortgage Porter

Subscribe to get the latest posts sent to your email.

If your loan officer says “federally registered” at the bottom of the NMLS page, then they are “registered” and not licensed (and not held to the same standards per the SAFE Act).