The SAFE Act was enacted in July 2008 to help create a national standard for residential mortgage originators. This is a fantastic idea EXCEPT that if a mortgage originator works for a depository bank, like Bank of America, Chase, Citi or Wells Fargo (just to name a few) they are excluded from licensing. Mortgage originators working for a bank will only have to be registered…and yes, there is a difference.

Archives for March 2010

If the Bank doesn’t charge an “overage or points”…what do you call this?

March 29, 2010 by 4 Comments

It really gets my goat when I see statements on the internet that are intended to lead the consumer to believe that someone or some institution is better than someone else…especially if the comment that is being spewed seems misleading to me.

Just a few moments ago on Twitter, a mortgage originator from Bank of America posted:

Bank of America DOES NOT CHARGE OVERAGES/POINTS to close Home Loans. Building trust with our customers is #1!

Her “tweet” also included a link to an article from Jack Guttentag which has me a bit riled and I’ll probably address soon in a separate post. [see update below].

Bank of America has changed their compensation program for their mortgage originators. It’s my understanding the mortgage originators are rewarded based on the volumes they originate. (I have serious concerns on how this is better for the consumer). This will continue to happen with banks and I believe that DFI is in the process of trying to do the same with mortgage originators who are licensed in Washington State. A consumer might assume that due to the tweet above, they’re paying less for a mortgage rate and perhaps should select this mortgage originator and/or the bank she works for.

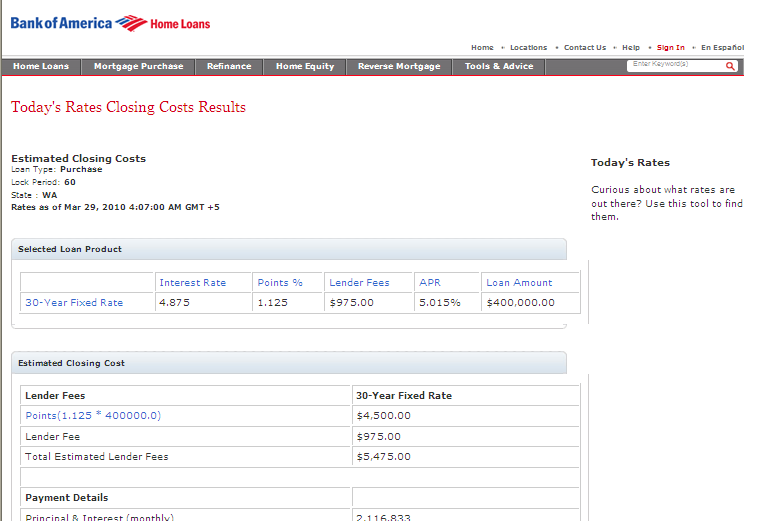

I decided to check out Bank of America’s website to price a rate based on the same criteria I used this morning. Their rate for a 30 year fixed mortgage in Seattle was not only 0.125% higher in fees, it’s also 0.125% higher in RATE than what I quoted hours ago.

This clearly states 1.125% in points to be paid for a 30 year fixed at 4.875%. (click on image for a larger picture).

UPDATE: Here’s Jack Guttentag’s definition of an overage, per the article the Bank of America mortgage originator tweeted about:

It is the difference between the price a lender posts with its loan officers — which is the price the lender expects to receive — and the price the loan officer charges the borrower. If the posted price is 5 percent and zero points, for example, and the loan officer charges the borrower 5 percent and half of a point, the half-point is the overage

Perhaps it’s an overage only if the mortgage originator is compensated the gain? What if it’s the bank who’s gaining the overage–is it okay to have the consumer pay more then? Banks are…well…banking it.

Consumers need to continue to be aware and to be responsible for their personal financial interest.

Hold Everything! What is Your Title Company’s Recording Protocol?

March 25, 2010 by Leave a Comment

If you’re a long time reader of The Mortgage Porter, you know that my pre-mortgage career was in the title and escrow industry. One of my early jobs was preparing documents to be recorded at King County. Later in my career, as a sales rep, I would sometimes have the opportunity to “be a hero” by driving “rush recordings” directly to the court house in Seattle and either meeting the title company’s recorder or actually having to “walk on” the documents myself. Recordings are the deeds and deeds of trust that will be recorded at the county to become public record to give the world notice that you now own the land or have debt attached to the property. (It also gives scammers notice to hound you with loan and other offers).

If you’re a long time reader of The Mortgage Porter, you know that my pre-mortgage career was in the title and escrow industry. One of my early jobs was preparing documents to be recorded at King County. Later in my career, as a sales rep, I would sometimes have the opportunity to “be a hero” by driving “rush recordings” directly to the court house in Seattle and either meeting the title company’s recorder or actually having to “walk on” the documents myself. Recordings are the deeds and deeds of trust that will be recorded at the county to become public record to give the world notice that you now own the land or have debt attached to the property. (It also gives scammers notice to hound you with loan and other offers).

On a recent transaction, I learned that all title companies are not the same when it comes to how the manage their recordings. When a title company receives documents from the escrow company, they are typically “on hold” meaning–do not record yet; or they’re a “walk on” which means, record as soon as possible. It’s my understanding that most title companies keep holds at King County UNLESS they have verified with the escrow company that the documents are not scheduled to close for some time.

This transaction involved a title company who apparently keeps recordings for King County at their Lynnwood office until they know they are released for recording and then they are sent with their recording courier. Problems can arise when recordings are released later by escrow or if the courier faces high volumes of traffic with her commute to Seattle (what are the odds of that?). I have been informed by their Senior Title Officer that they are changing their policy on keeping holds at their office.

It could be worth asking your preferred King County title provider:

Where do they keep recordings that are on hold?

Will they do a special courier to the court house if needed? (a title rep can do this)

Hopefully the recordings are kept at King County (or the appropriate county) so that in the event of a later release, the documents are prepared and ready to go to avoid delays with closings.

Related Post:

What Takes Place Between Signing and Closing

The Pacific Northwest Housing Summit and Seattle RE Barcamp

March 21, 2010 by Leave a Comment

Hard to believe after months of planning, the Pacific Northwest Housing Summit and Seattle RE Barcamp events are done.

During the Housing Summit, I brought my netbook and provided a stream of updates via my Mortage Porter Twitter account and for PNWHS on Twitter. Overall I was very pleased with the event–there was a lot of good information (not all positive) shared with what to expect with housing in our area. The wrap-up post on the Housing Summit site will continue to be updated with articles as I find them. I was a bit disappointed that more real estate professionals did not show up for the event. I'm chalking it up to it being a reflection of the current state of our industry…especially mortgage originators. It's true that there were not continuing education clock hours valuable for LO's due to the NMLS requirements, but I don't that's reason enough to not attend an event like this. I wonder how many are planning to stick around in this industry as the bar continues to raise and disclosure forms continue to pile on. The job is much tougher than what it used to be and if the Fed (and big banks) have their way, our income will be reduced to peanuts. Good luck finding an experienced mortgage originator to assist you with your largest investment…sorry…didn't mean to digress!

Seattle RE Barcamp was a blast. I enjoyed really enjoyed volunteering for this event and strongly encourage others to do the same. Since it followed the Housing Summit, there were topics suggested that were beyond social media as I had hoped.

Seattle RE Barcamp was a blast. I enjoyed really enjoyed volunteering for this event and strongly encourage others to do the same. Since it followed the Housing Summit, there were topics suggested that were beyond social media as I had hoped.

My only regret is that I couldn't attend more sessions! PS… if you have any photos or videos from the event, feel free to post them at the Flickr group.

We had folks from all over the country join us at the Seattle Center on last Thursday and Friday for the Housing Summit and RE Barcamp. I really enjoyed finally meeting Frank Garay and Brian Stevens from Think Big Work Small. I appreciate their efforts in keeping mortgage professionals up-to-date with current issues facing our industry laced with humor on their vlog.

Thank all of you for making both these events so special!

I hope to see you at The Pacific NW Housing Summit & Seattle RE Barcamp

March 13, 2010 by Leave a Comment

The Pacific NW Housing Summit and RE Barcamp Seattle are taking place this week on Thursday, March 18 and Friday, March 19, 2010. If you are in any aspect of the real estate industry, I hope to see you at both events!

Gifts from the Bank of Mom and Dad – Part 2: Conventional Financing

March 12, 2010 by 2 Comments

Often times when gifts from family members are involved, borrowers my opt to use FHA financing since the guidelines are (currently) more flexible than conventional with regards to gifts. With FHA, a gift from a family member can go towards to borrowers minimum required investment with conventional financing, it cannot.

Here’s an example. Let’s say we have a sales price of $265,000 with 10% down payment creating a loan amount of $238,500. Once you factor in estimated closing costs of $2,400 and and prepaids/reserves of $3,100; the amount due at closing is roughly $32,000 (10% down = $26,500 + $2,400 + $3,100). The borrowers also have a $5,000 contribution towards closing costs from the seller.

At this loan to value, with conventional financing requires that the borrower invests a minimum of 5% of their own personal funds into the transaction. Unlike FHA, these funds cannot be gifted from the family members. NOTE: if the gift is 20% down or more, the 5% rule for conventional financing does not apply (the whole down payment can be gifted).

Staying with our example, this means that the borrower must contribute 5% of $265,000 of their “seasoned” funds = $13,250.

With the amount due at closing at $32,000, the borrower must contribute at least $13,250 (5% of the sales price) of their own funds towards the $32,000 (10% down payment). This leaves $18,750 remaining “due at closing”. The borrowers earnest money check (if sourced – meaning documented as being their own funds) can count towards the 5% investment requirement and so can deposits with the mortgage company. For example, the our borrowers submitted an earnest money check in the amount of $5,000 with their purchase and sales agreement, they would have $8,250 remaining to invest into the transaction of the 5% requirement ($13,250 – $5,000 = $8,250).

Once the borrower meets the 5% down payment, the gift and any seller credits can be applied towards the transaction. A seller contribution can only go towards allowable closing costs and prepaids. With this scenario, that totals $5,500 ($2,400 + $3,100). The seller cannot contribute more than $5,500 (actual closing costs and prepaids).

Unlike a seller contribution, the gift from parents can be applied towards down payment or closing costs/prepaids, once the borrower’s 5% investment is met. If your gift from the parents is larger than the remaining amount due at closing, you can either reduce your loan amount or not use the entire gift. NOTE: Your parents may want to check with tax adviser regarding possible tax implications with gifting funds.

With FHA financing, their is also a minimum required investment from the borrower, which is currently 3.5% of the sales price. A gift from parents CAN be applied towards the borrowers minimum required investment (the 3.5%).

When parents provide a gift with conventional or FHA financing, they need to be prepared to provide documentation of where the funds came from. They will sign a gift letter and provide a recent bank statement showing that the funds are available. There also needs to be a “paper trail” documenting the transfer of the gift funds (photo copy EVERYTHING–you’re better off having too much paper work to provide your mortgage originator than not enough).

If you have questions about financing a home located in Washington State, please contact me, I’m happy to help! We have both FHA and conventional programs available.

Related post: Gifts from the Bank of Mom and Dad – Part 1: FHA

FHA Flips for Flipped Homes (Some Restrictions Apply)

March 11, 2010 by Leave a Comment

UPDATE: HUD HAS EXTENDED THIS WAIVER THROUGH DECEMBER 2014. Information in this post from March 2010 may be outdated – as are many blog posts about mortgages (thanks to our ever changing guidelines).

I recently shared with you some of the upcoming changes to FHA insured loans that were addressed in a letter from HUD’s David Stevens. In this letter, he reminds readers that FHA has recently “waived the regulation that prohibits the use of FHA financing to purchase properties that are being resold within 90 days of previous acquisition”.

Due to previous FHA guidelines, investors who purchased homes to renovate and resale in a short period of time (90 days), would not be able to accept an offer from an FHA buyer. They were limited to cash buyers or those who qualified with conventional financing. From Stevens:

“During this period of high foreclosures, FHA wants to encourage investors that specialize in acquiring and renovating properties to renovate foreclosed and abandoned homes for homebuyers. Our aim is to help stabilize real estate prices as well as neighborhoods and communities where foreclosure activity has been high. The waiver is applicable to all properties being resold within the 90-day period acquisition and is not limited to foreclosed properties.”

The waiver takes effective February 1, 2010 and not every flipped home will qualify. Per the Waiver of Requirements:

- All transactions must be arms-length with no identity of interest between buyer and seller or other parties participating in the sales transaction.

- If the sales price of the property is 20% or more above the seller’s acquisition cost be prepared for extra scrutiny. A second appraisal will be likely required as well as an inspection ordered by the lender.

The waiver is set to expire one year, unless it is extended or withdrawn from the Commissioner. More information is expected to follow from a HUD Mortgagee Letter.

Currently, the FHA loan limits for single family residences in King, Pierce and Snohomish counties is $567,500. FHA mortgage insurance is set to increase on case numbers issued April 5, 2010 and later. And this summer, the amount a seller can contribute to allowable closing costs will be reduced from 6% to 3%.

I won’t mention that the Home Buyer Tax Credit is expiring in 50 days on April 30, 2010 (oops…guess I just did)!

If you would like a rate quote for an FHA insured mortgage for homes located anywhere in Washington, please click here. I have been originating FHA mortgages at Mortgage Master Service Corporation since April 2000 and I’m happy to help you.

Friends Don’t Let Friends Miss Out on THE Premier Real Estate Event in Seattle

March 6, 2010 by Leave a Comment

The Pacific Northwest Housing Summit and Seattle RE Barcamp 2010 are less than two weeks away!

It's time to rsvp to both events, if you haven't done so all ready. Preregistration for the Pacific Northwest Housing Summit will save you $10! RE Barcamp is free–but knowing how many folks to expect before the event is very helpful.

If you are in any aspect of the real estate industry–you don't want to miss out on either of these events.

I look forward to seeing you March 18th and 19th at the Seattle Center!

Recent Comments