HUD has a requirement that in order for a borrower to do a streamline refinance their existing FHA mortgage, their scenario must have a “net tangible benefit”. FHA streamline refinances are popular today because they do not require an appraisal and FHA mortgage rates are very low.

HUD wants to make sure that the refinance makes sense and that it will actually benefit the borrower. Net tangible benefit requirements were created to protect home owners from refinancing when it doesn’t pencil out by HUD’s standards. For example, a borrower’s proposed mortgage payment (principal, interest and mortgage insurance) must be reduced by 5% or it will not meet the “net tangible benefit” requirement for refinancing a fixed rate to fixed rate FHA streamline refi.

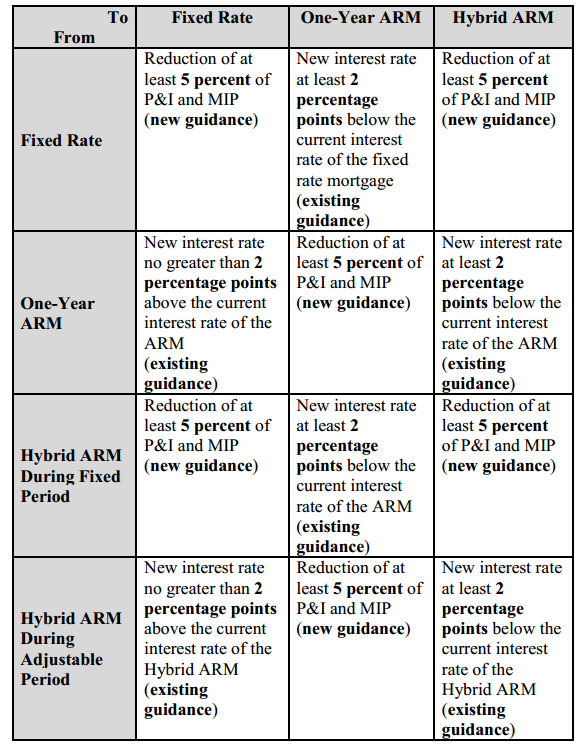

Here is HUD’s Net Tangible Requirement chart.

FHA Net Tangilbe Benefit

It all sounds pretty good until you’re the borrower who isn’t being allowed to refinance due to not meeting a net tangible benefit.

Here’s an examples of King County home owner trying to refinance their FHA mortgage. NOTE: rates quoted are from Friday, November 16, 2012. Mortgage rates change often. If you would like your personal rate quote for your home located anywhere in Washington state, click here.

Roger Renton has an FHA high balance mortgage that he obtained in 2010 (past the FHA cut off date for reduced mortgage insurance on his new refi) which currently has a rate for his 30 year fixed of 4.500%. He would like to do an FHA streamline refinance which would drop his rate over a full point to 3.250% (apr 4.119).

Roger’s current PIMI (principal, interest and mortgage insurance) payment is $2,982.44 (p&i of $2741.44 plus monthly mortgage insurance of $240). In order for Roger to be able to meet net tangible benefits, his new propose mortgage payment must be reduced by 5% or $149.12 to $2,757.52 (or lower).

At 3.250% (apr 4.119) Roger’s proposed PIMI payment is $2,857.32 (p&i of $2,317.21 with mortgage insurance of $540.11). Although Roger would save $125.12 each month, unless his PIMI is below $2,833.22, HUD will not permit this FHA streamline refi. Roger could opt to pay his FHA upfront funding fee as a closing cost and bring cash in roughly $18,000 to reduce the proposed loan amount in order to meet the net tangible benefit requirement and have a proposed PIMI of $2757.52.

NOTE: If Roger Renton’s existing FHA mortgage was guaranteed by HUD prior to June 1, 2009, then his proposed mortgage insurance would be dramatically reduced.

What if Roger wanted to do an FHA streamlined refi converting his 30 year to a 15 year? Even though he’d drop his rate to 2.750% (apr 3.319) and would be shaving years off his mortgage, it does not currently pass the net tangible benefit test of reducing his payment by 5% or more. Although the mortgage insurance with a 15 year is greatly reduced compared to the 30, the principal and interest is higher creating a PIMI payment of $3,867.76.

Even if Roger Renton easily qualifies for the 15 year fixed FHA streamlined mortgage payment – he’s not permitted to have this program using an FHA streamlined refi under HUD’s current guidelines.

I’ve voiced my opinions about net tangible benefit before on this blog. I do hope that HUD will adjust their guidelines soon. Net tangible benefit is preventing a lot of FHA borrowers from the opportunity to reduce their mortgage payments or to reduce their mortgage terms.

Discover more from The Mortgage Porter

Subscribe to get the latest posts sent to your email.

Thank you for posting this article. My husband and I are currently going through this same thing right now.

We are trying to get a 15 year loan, but do not qualify due to the benefit to borrow test. It’s sad when people are trying to benefit themselves by drastically lowering their mortgage, but cannot because of ridiculous guidelines!

But now if we needed help because we could not afford out mortgage, there are plenty of loans and help for that, but no help for those trying to better themselves….