Did you know that if your existing mortgage is FHA on your investment property, that it may qualify for an FHA streamlined refi?

Here’s the scoop for a non-owner occupied FHA streamlined refi:

Helping Washington State homeowners learn more about their mortgage options.

Did you know that if your existing mortgage is FHA on your investment property, that it may qualify for an FHA streamlined refi?

Here’s the scoop for a non-owner occupied FHA streamlined refi:

HUD has scheduled another increase to FHA annual mortgage insurance premiums effective with new case numbers obtained April 1, 2013 and later. FHA’a annual mortgage insurance premiums are paid monthly and are set to rise by 10 basis points.

For example, a base loan amount of $400,000 with a loan to value of 95% or lower, currently has a monthly mortgage insurance premium of $396.65 based on a rate of 1.20%. After the new mortgage insurance rates go into effect, this monthly premium will be $429.71 – an increase of $33.06 per month.

NOTE: Home owners who currently have FHA insured mortgages for their primary or investment properties and who had those mortgages guaranteed by FHA prior to June 1, 2009 will still qualify for reduced mortgage insurance premiums with FHA streamlined refinances. If you’re not one of these lucky home owners, you may want to take action now!

In addition, with new FHA loans as of June 3, 2013, FHA mortgage insurance will remain on the life of the loan. The only way to terminate it is to refinance out of an FHA loan or pay the loan off. Currently, FHA annual mortgage insurance is set to drop off the loan after it reaches a 78% loan to value and a minimum of 60 mortgage payments have been made. However with a minimum down payment scenario, it often takes closer to nine years before the loan to value reaches 78%. I would bet that many Washington home owners either refinance or sell their homes before their mortgage insurance drops off. Regardless, if you want to avoid having to pay FHA mortgage insurance for the life of that FHA insured mortgage, you’ll need to have your FHA case number prior to June 3, 2013.

What can you do?

If you want to avoid having a higher mortgage payment and you’re considering an FHA loan for your refinance or home purchase, you have a short window of opportunity to secure your lower payment now. An FHA Case number is not your application date. It is actually obtained shortly after you have a bona fide transaction and application. As we near the April 1 date, if you have a new FHA mortgage in process, you will want to confirm with your mortgage professional that your FHA case number has been secured. (They can provide you your FHA case number as proof).

I have been helping people with FHA insured mortgages since April 2000 at Mortgage Master Service Corporation. If you would like me to provide you with a rate quote for your home located anywhere in Washington State, click here.

I’ve been writing about pending changes to FHA insured mortgage loans regarding the mortgage insurance premiums. Yesterday, HUD issued Mortgagee Letter 2013-04 which makes the proposed changes “official”.

We’ve been anticipating changes to how long mortgage insurance will remain on an FHA insured loan as well as increases to FHA’s mortgage insurance premiums.

It’s no surprise that FHA will increase annual mortgage insurance premiums (paid monthly). The first increase goes into effect with case numbers issued April 1, 2013 and later.

NOTE: in the Seattle – King County area, FHA jumbos are loan amounts from $417,001 to $567,500.

But wait… there’s more!!

Effective on case numbers issued June 3, 2013 and later, 15 year fixed FHA mortgages with a loan to value of 78% or lower will have annual mortgage insurance of 45 bps. Currently these loans have zero annual mortgage insurance.

Want to save on your FHA mortgage insurance? Act quickly!! Click here for a mortgage rate quote for homes located anywhere in Washington state.

FHA streamlined refi’s where the current FHA mortgage was endorsed prior to June 1, 2009 are exempt from this adjustment. These loans still qualify for reduced mortgage insurance premiums.

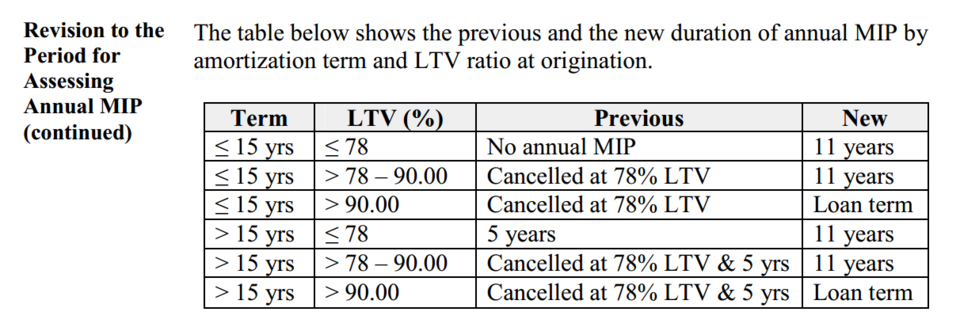

Per the mortgagee letter, this will be effective on case numbers issued June 3, 2013 and later, FHA insured mortgages will change when mortgage insurance can be terminated. Most FHA loans will have mortgage insurance for the term of the mortgage for loans with case numbers issued June 3, 2013 and later.

Here is a chart from HUD comparing “previous” (in effect now until the new regulation) and “new” (in effect with case numbers issued June 3, 2013 and later).

If you are considering an FHA insured mortgage and would like to have mortgage insurance that one day drops from your mortgage payment – you have a couple months left to do so. The FHA Case number is typically (but not always) ordered at application.

I am happy to help you with your FHA purchase or refinance on your home located anywhere in Washington state. I have been originating mortgages at Mortgage Master Service Corporation since April 2000, including FHA loans.

EDITORS NOTE: This post was written in 2013. FHA loan limits have changed as well as the interest rates posted below. Please see the bottom of this web page for current FHA loan limits. If I can provide you with a current rate quote for your home in Washington, please click here.

EDITORS NOTE: This post was written in 2013. FHA loan limits have changed as well as the interest rates posted below. Please see the bottom of this web page for current FHA loan limits. If I can provide you with a current rate quote for your home in Washington, please click here.

If you are considering buying a duplex, triplex or fourplex and you’re going to live in one of the units, FHA is a possible mortgage option.

Today HUD issued a press release confirming pending changes to help bolster FHA’s capital reserves.

“These are essential and appropriate measures to manage and protect FHA’s single-family insurance programs” said Galante. “In addition to protecting the MMI Fund, these changes will encourage the return of private capital to the housing market, and make sure FHA remains a vital source of affordable and sustainable mortgage financing for future generations of American homebuyers.”

Some of the changes to take place with HUD have already been announced. Here are a few points from today’s press release

We are waiting for HUD to issue Mortgagee Letters before this goes into effect.

Stay tuned!

I’m working with a couple in Seattle who would like to buy a home. They have excellent credit (scores of 740 or higher) and are planning on using $70,000 for their down payment and closing cost. They want to know how much home they can buy based on their down payment.

The following rate quotes are effective as of January 24, 2013 at 12:20 pm. Rates change constantly, for your personal rate quote for a home located in Washington state, click here.

Conforming High Balance allows them to buy a home priced at $576,000.

The conforming loan limit in Seattle/King-County is currently $506,000. Using a conventional mortgage, they could buy a home priced at $576,000.

Current mortgage rates for a 30 year fixed conforming high balance ($417,001 – $506,000) based on this scenario is 3.750% (apr 4.094).

3.750% is priced as close to “par” as possible meaning there is as little rebate credit or discount points priced with the interest rate. We could adjust the rate slightly higher to create more rebate credit to help pay for closing cost or we could reduce the rate by paying more in discount points.

The loan to value based on a sales price of $576,000 and loan amount of $506,000 is 87.874% which means the Seattle home buyers will have private mortgage insurance (pmi). For this client, we’re opting to include the pmi in their mortgage payment instead of paying it as an upfront additional closing cost or doing “split premium” mortgage insurance.

The principal and interest payment is $2,343.36 plus private mortgage insurance of $282.52 gives us a “PIMI” payment of $2,625.88. Property taxes and home owners insurance are additional.

The Seattle home buyers will negotiate the seller paying for remaining closing cost and prepaids/reserves estimated at $7900, leaving their amount due at closing very close to $70,000. If the sellers opt to not pay for closing cost and prepaids, the buyers can use rebate pricing (slightly increasing the mortgage rate) to offset the cost.

FHA allows them to buy a home priced up to $637,500.

FHA mortgages in the Seattle/King County area have a loan limit of $567,500. With a down payment of $70,000 they could buy a home priced up to $637,500. The big difference between FHA and conventional financing is the mortgage insurance. FHA has both upfront and monthly mortgage insurance.

The current mortgage rate I’m quoting for their FHA scenario is 3.375% (apr 4.059%).

This rate is priced with a little more rebate to help reduce closing cost. If the Seattle home buyers want a lower rate with less rebate credit, they certainly can opt for that. Mortgage rates are not locked until we have a bona fide contract and the rates will be “floating” while they shop for a home.

The principal and interest on this rate and loan amount is $2,552.80 with mortgage insurance at $562.43 providing a PIMI payment of $3,115.23. Property taxes and home owners insurance are additional.

After the rebate credit, if the buyers negotiate the seller paying the remaining balance of their closing cost, prepaids and reserves in the amount of $4,000, the buyers will need around $70,000 for funds due at closing.

VA loans allow them to purchase up to $780,000 with a “VA Jumbo” loan.

The VA zero down loan limit in Seattle is $500,000. When a loan amount exceeds the limit, eligible Veterans can have a down payment based 25% off the difference between the sales price and loan amount.

For example, a sales price of $780,000 less $500,000 loan limit = $280,000. $280,000 x 25% = $70,000 down payment.

The current rate I’m quoting for this VA Jumbo 30 year fixed loan is 3.250% (apr 3.379).

The principal and interest payment on this loan is $3,136.31. There is no mortgage insurance on a VA loan. Property taxes and home owners insurance are additional.

If the seller pays for $4500 of the Veteran’s closing cost and prepaids, then the amount due at closing will be around $70,000.

USDA loans are not eligible in the Seattle area because it’s not a rural area.

If you are interested in buying a refinancing a home located anywhere in Washington state, I’m happy to help you. I’ve been originating residential mortgages at Mortgage Master Service Corporation since April 2000.

HUD has confirmed that 2013 FHA loan limits will remain unchanged from 2012.

King County, Snohomish County and Pierce County

- 1 Unit: $567,500

- 2 Unit: $726,500

- 3 Unit: $878,150

- 4 Unit: $1,091,351

Benton and Franklin Counties:

- 1 Unit: $275,000

- 2 Unit: $352,050

- 3 Unit: $525,550

- 4 Unit: $528,850

Chelan and Douglas Counties:

- 1 Unit: $342,700

- 2 Unit: $438,700

- 3 Unit: $530,300

- 4 Unit: $659,050

Clallam County:

- 1 Unit: $384,100

- 2 Unit: $491,700

- 3 Unit: $594,350

- 4 Unit: $738,650

Clark and Skamania Counties:

- 1 Unit: $418,750

- 2 Unit: $536,050

- 3 Unit: $648,000

- 4 Unit: $805,300

Island County:

- 1 Unit: $381,250

- 2 Unit: $488,050

- 3 Unit: $589,950

- 4 Unit: $733,150

Jefferson County:

- 1 Unit: $437,500

- 2 Unit: $560,050

- 3 Unit: $677,000

- 4 Unit: $841,350

Kitsap County:

- 1 Unit: $475,000

- 2 Unit: $608,100

- 3 Unit: $735,050

- 4 Unit: $913,450

Kittitas County:

- 1 Unit: $328,750

- 2 Unit: $420,850

- 3 Unit: $508,700

- 4 Unit: $632,200

Mason County:

- 1 Unit: $310,000

- 2 Unit: $396,850

- 3 Unit: $497,700

- 4 Unit: $596,150

San Juan County:

- 1 Unit: $593,750

- 2 Unit: $760,100

- 3 Unit: $918,800

- 4 Unit: $1,141,850

Skagit County:

- 1 Unit: $373,750

- 2 Unit: $478,450

- 3 Unit: $578,350

- 4 Unit: $718,750

Thurston County:

- 1 Unit: $361,250

- 2 Unit: $462,450

- 3 Unit: $559,000

- 4 Unit: $694,700

Whatcom County:

- 1 Unit: $375,000

- 2 Unit: $480,050

- 3 Unit: $580,300

- 4 Unit: $721,150

Adams, Asotin, Cowlitz, Ferry, Garfield, Grant, Grays Harbor, Lewis, Lincoln, Okanogan, Pacific, Pend Oreille, Spokane, Stevens, Whakiakum, Walla Walla, Whitman and Yakima Counties:

- 1 Unit: $271,051

- 2 Unit: $347,009

- 3 Unit: $419,425

- 4 Unit: $521,250

Related post: 2013 Conforming Loan Limits for Washington State

HUD recently announced they will extend the “anit-flip waiver” through December 2014. Without this waiver, home buyers would not be able to use FHA financing for homes that are considered being “a flip” ( a property that is quickly resold at a much higher price).

Prior to the waiver, a mortgage was not eligible for FHA insurance if the contract of sale for the purchase of the property that secured the mortgage was executed within 90 days of the prior acquisition by the seller, and the seller did not come under any of the exemptions to this 90-day period specified in the regulation.

Through the regulatory waiver, FHA encourages investors that specialize in acquiring and renovating properties to renovate foreclosed and abandoned homes, with the objective of increasing the availability of affordable homes for first-time and other purchasers, helping to stabilize real estate prices as well as neighborhoods and communities where foreclosure activity has been high. The waiver is applicable to all single family properties being resold within the 90-day period after prior acquisition, and is not limited to foreclosed properties. Additionally, the waiver is subject to certain conditions, and mortgages must meet these conditions to be eligible for the waiver.

The Waiver continues to be limited to sales meeting the following conditions:

When a home is being resold 20% or higher than what the seller purchased the property for in less than 90 days, often times a second appraisal will be required and the seller will need to show documentation to support the increased value in the home, such as receipts for the improvements made. A property inspection report will also be required by the lender to assure the quality of the improvements made to the property. Any health or safety issues disclosed by the property inspection will need to be corrected.

If a home has been re-sold withing 91-180 days at more at 100% or more than the seller’s acquisition cost, the same conditions will apply.

NOTE: If a second appraisal is required, the home buyer is not allowed to pay for it per HUD. And you can pretty much count on that second appraisal being required. Thanks to LO Comp being passed by the Fed in 2010, your friendly mortgage professional is not allowed to pay for the appraisal either.

Investors (aka Flippers) who are reselling in a short period of time for a much higher amount than their acquisition cost should be prepared for the cost of the second appraisal when the buyer is using a FHA mortgage for financing. They should also retain detailed records of improvements (including all receipts) when they’re planning to quickly resale a home. The seller’s acquisition cost is the sales price of the home, plus the seller’s closing cost, including real estate commissions. It does not include any repairs.

If you are considering buying a home located anywhere in Washington State, I’m happy to help you! Click here for a mortgage rate quote for homes located anywhere in Washington. I’ve been originating home loans at Mortgage Master Service Corporation since April 2000, including FHA insured loans.

![]() Rhonda Porter is a Licensed Mortgage Originator MLO121324 living in the greater Seattle area. Rhonda began her career in 1986 in the title and escrow industry and began her mortgage career in 2000. She enjoys helping people understand the mortgage process and started writing The Mortgage Porter in late 2006. Read More…

Rhonda Porter is a Licensed Mortgage Originator MLO121324 living in the greater Seattle area. Rhonda began her career in 1986 in the title and escrow industry and began her mortgage career in 2000. She enjoys helping people understand the mortgage process and started writing The Mortgage Porter in late 2006. Read More…

Recent Comments