Sometimes an employment opportunity may become available while you’re in the process of buying a home or refinancing. Lenders are looking at a borrowers employment and income stability so depending on the type of field you’re in, a change of employment may or may not impact your loan approval. [Read more…]

How Often Will You Have to Provide Documents During the Mortgage Process?

April 5, 2012 by 1 Comment

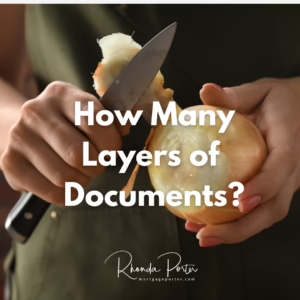

I’ve often thought that the loan process for a borrower is similar to peeling an onion. At the very beginning stages, when a borrower is considering obtaining a mortgage and they discuss their scenario with their mortgage originator, they appear to be a smooth, shiny Walla Walla Sweet. As the process continues, more layers are removed as documentation is provided. Sometimes when several layers have been peeled away, you no longer have an onion or at least, not the one you originally started with. It’s crucial that a mortgage originator takes an in-depth interview with their clients before they enter into a transaction (purchase or refinance) to make sure as much their financial information has been addresses as possible. There may be a significant difference between how a borrower views their financial scenario and what their supporting income and asset documents tell to an underwriter. [Read more…]

I’ve often thought that the loan process for a borrower is similar to peeling an onion. At the very beginning stages, when a borrower is considering obtaining a mortgage and they discuss their scenario with their mortgage originator, they appear to be a smooth, shiny Walla Walla Sweet. As the process continues, more layers are removed as documentation is provided. Sometimes when several layers have been peeled away, you no longer have an onion or at least, not the one you originally started with. It’s crucial that a mortgage originator takes an in-depth interview with their clients before they enter into a transaction (purchase or refinance) to make sure as much their financial information has been addresses as possible. There may be a significant difference between how a borrower views their financial scenario and what their supporting income and asset documents tell to an underwriter. [Read more…]

5 Ways to Derail Your Loan Approval

January 27, 2011 by 2 Comments

You’re getting ready to buy a home or refinance your home with your closing day around the corner when your mortgage originator contacts you to let you know there may be a problem. Some issues may not revealed until days or sometimes weeks into a transaction. Anytime documentation is provided to the mortgage company, it has the potential to raise more questions or require more documentation to satisfy underwriting guidelines. Here are five situations to be aware of that can cause headaches during the loan process.

You’re getting ready to buy a home or refinance your home with your closing day around the corner when your mortgage originator contacts you to let you know there may be a problem. Some issues may not revealed until days or sometimes weeks into a transaction. Anytime documentation is provided to the mortgage company, it has the potential to raise more questions or require more documentation to satisfy underwriting guidelines. Here are five situations to be aware of that can cause headaches during the loan process.

Do I Really Have to Provide All Pages of My Bank Statements?

October 29, 2009 by 1 Comment

When assets are being used for down payment of a new home, towards closing costs on a refinance or even to document that the borrower has enough reserves (typically a couple months of mortgage payments) in the bank after closing; they need to be documented.

When assets are being used for down payment of a new home, towards closing costs on a refinance or even to document that the borrower has enough reserves (typically a couple months of mortgage payments) in the bank after closing; they need to be documented.